RISING RATES AND GOLD – THE MYTH

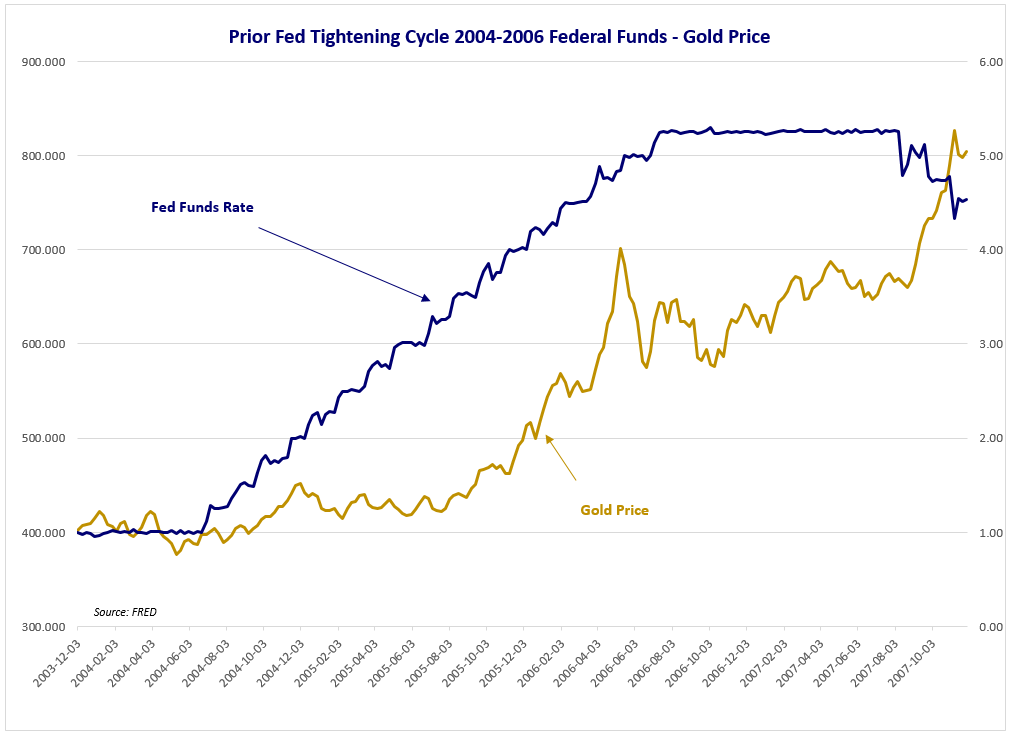

The timing of when the Fed is going to begin raising the Fed Funds Rate has been the Market focus for some time now. Last week Cleveland Federal Reserve President, Loretta Mester, stated she wanted June to be a “viable option” for an interest rate hike followed by St. Louis Fed President, James Bullard, commenting it was time to remove “patient” from Fed minutes and move rates above zero. Fed Chair Janet Yellen in her congressional testimony this week defined patient as being two FOMC meetings. Perhaps the Fed will raise rates this year in the face of global economic headwinds. The Fed’s effort to prime the market for an interest rate increase is twofold; first to maintain some semblance of policy credibility and second to avoid a flash crash becoming more than a flash. For the gold market, the specter of rising rates has successfully kept investors on the sideline as investment banks maintain the constant mantra rising rates are bad for gold prices perpetuating the myth.

The chart below shows gold price action the last time the Fed went through an interest rate hike cycle in 2004 to 2006 with the gold price rising as rates went higher. No doubt, the removal of uncertainty is a bullish factor for the gold market.

Negative Rates – Crazy Stuff

There is now €1.5 trillion of Eurozone government debt with maturities over a year with negative rates – you pay them so they can owe you. Crazy stuff. QE is to blame we are told as the ECB steps up purchases of sovereign debt. It is difficult to comprehend the rational in the market place as the “race to debase” would seem to preclude a move to lower rates, let alone negative rates. We can understand gold has a negative carry because of the cost to store and it is not subject to default because it is not someone else’s liability. A negative carry on government debt with a history of default and debasement seems incongruent with common sense. Perhaps negative rates all come down to capital flows and the commoditizing of government debt for collateral purposes. However, there would seem to be a point of rising risk that may lead to an “Aha” moment that tilts in the favor of owning gold as the preferred alternative to owning government debt.

China, India, and Apple

Is Apple set to join China and India as the largest consumers of gold over the next 12 months? According to reports, Apple’s new high end watch set to launch in the second quarter of this year has approximately 2 ounces of gold in each watch. Estimates put forward are for upwards of one million units per month with Asian buyers the big market. Simple math: 746 tons of potential gold demand in a twelve month period, putting it on par with demand from China and India and almost equaling the amount of gold held in the SPDR Gold Trust (GLD). An added demand component in an already tight physical bullion market can be nothing but bullish for gold prices.

Return of the Value Investor to the Gold Mining Space?

The BMO Metals Conference was held this past week in Florida. Mining companies presented to institutional investors in quick 30 minute meetings – basically a speed dating set-up. The most interesting aspect of the conference were the number of value shops looking at the space. There is growing recognition that the gold mining industry is trading below replacement capital and that lower oil prices and currencies are a tail wind to an industry that has done a fair amount of heavy lifting when it comes to rationalizing cost structures and refocusing on capital discipline. Additionally, attendees were able to come away with the notion that over the next five years global mine supply is set to contract dramatically as there have been no major new discoveries and the next generation of gold mines will be smaller, but more profitable in order to meet higher minimum investment hurdles and account for geopolitical risk. The stage is being set for the gold industry to recapture some of its lost trading multiples to the gold price. See chart showing current value of HUI vs. Gold.

The NYSE Arca Gold BUGS Index is a modified equal dollar weighted index of companies involved in gold mining.

2137-NLD-3/16/2015