OCM Perspective – Rising Gold Market

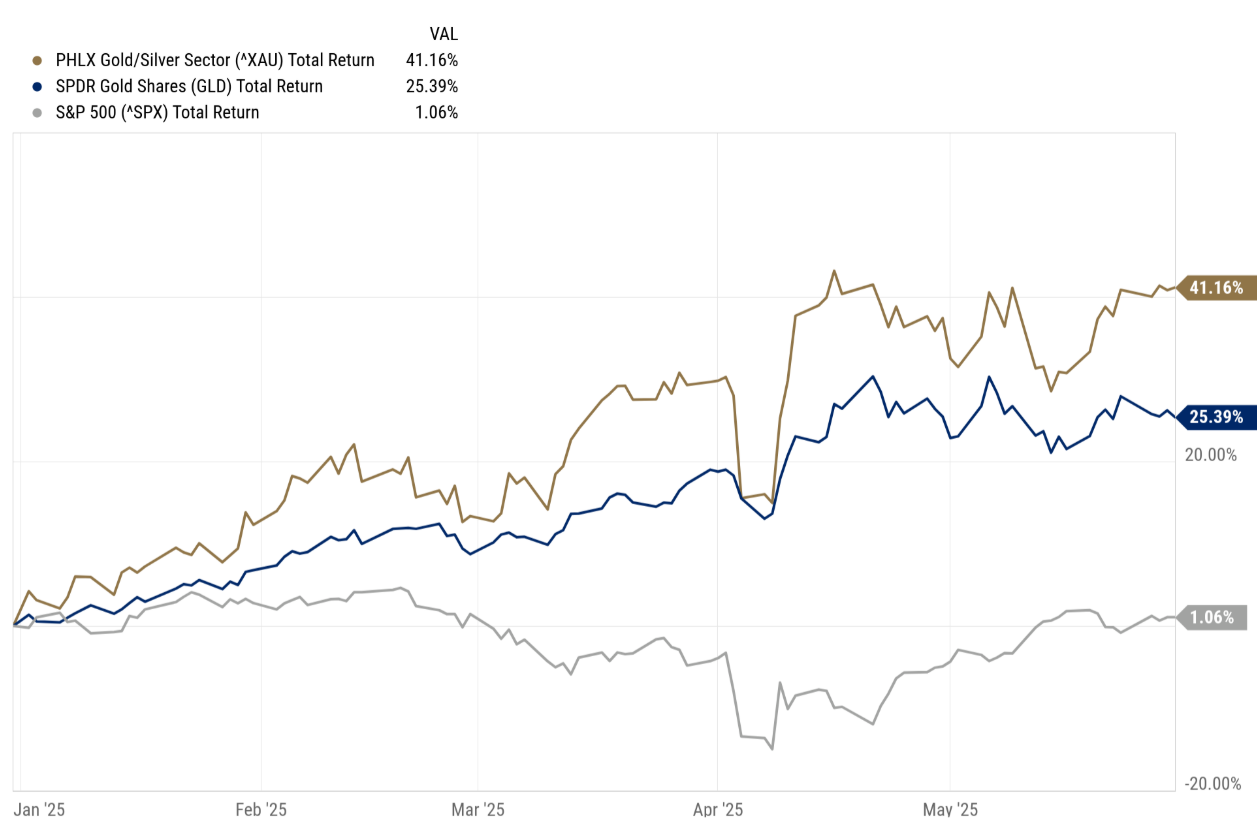

Physical gold and precious metal equities have enjoyed 2025, compared to the rest of the broader market. Below we outline several factors why we believe the sector has tailwinds for the foreseeable future.

Gold Miners Q2 Shaping up Nicely

The average gold price in Q2 through the first two months of the quarter is $3267, up about 14% from the Q1 average price received by most gold miners. Operating cost pressures have eased with oil prices trending lower over the quarter. The sector is on the verge of harvesting robust cash flow. The big question for precious metal investors and mining company board rooms is capital allocation. Dividends and/or share buybacks versus M&A and capex spend.

In the OCM portfolio we have seen increased cash dividend payouts by Lundin Gold, Endeavour Mining and AngloGold, among others. Newmont Mining and Dundee Precious Metals are among those companies aggressively buying back stock. As the gold price continues to consolidate above $3,000, we expect the broader market to appreciate the increased earnings and cash flow generation of the precious metals mining sector.

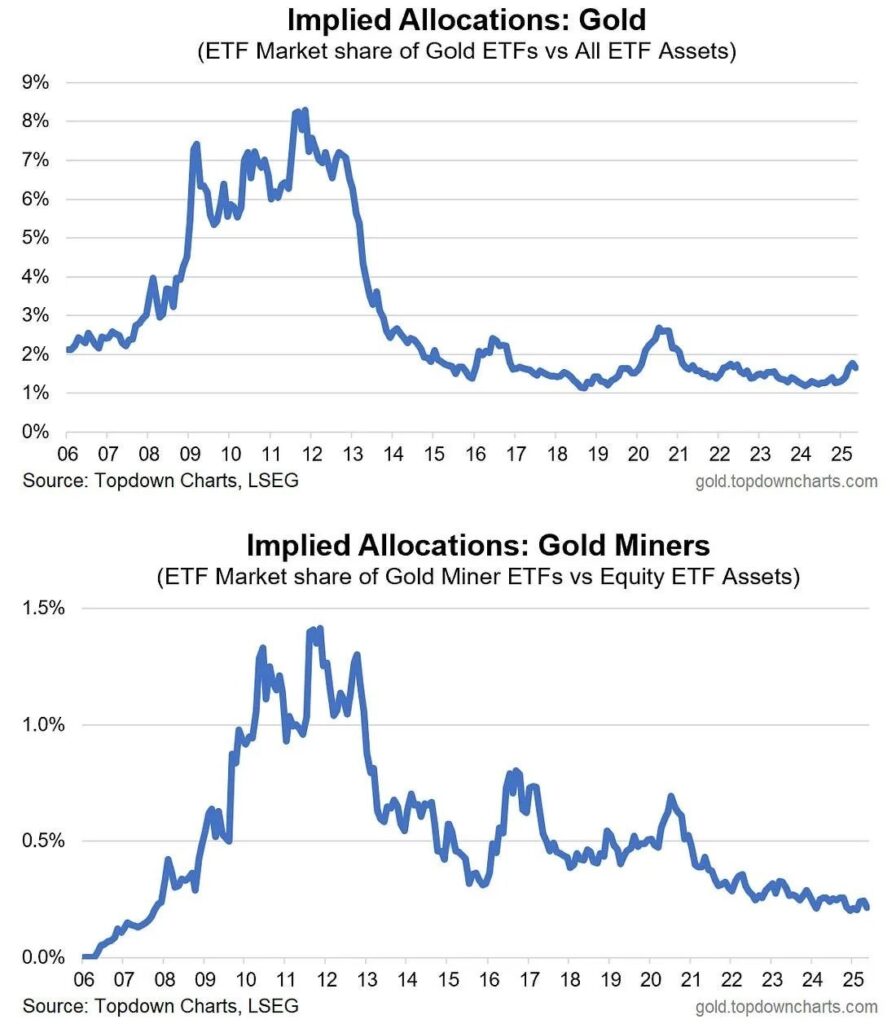

Capital Flows Remain Muted

Significant capital flows to the precious metals sector, in our opinion, will be driven by sector fundamentals standing out versus other market sectors. We expect this will happen once investor hope in Trump’s economic promises fade and thus leading to a broader market sell off. Based on ETF market share, gold bullion and gold miners are yet to see capital flows, especially the miners (see chart). The prospect for much higher valuations based on capital flows to the sector is real when compared to investor participation in previous precious metal bull run such as 2010 to 2012.

Trump’s Big Beautiful Bill

More of the Same – Big Debt

Trump’s tax and spending bill highlights that the president is pivoting away from spending cuts toward fiscal expansion to grow the economy. The long end of the treasury curve is displaying its displeasure by taking yields higher and now a debt crisis in the U.S. is becoming a real possibility as fiscal solvency narrative gains traction.

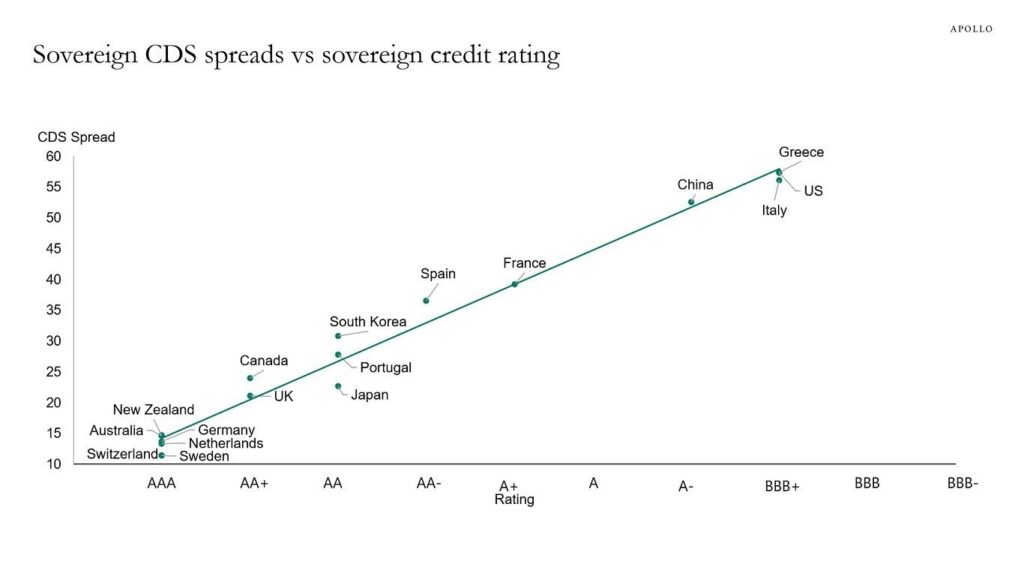

Moody’s Downgrades U.S. Debt

Last month Moody’s downgraded U.S. credit rating by one notch leaving no credit agencies rating U.S. debt triple A. Credit default swaps (CDS) spread are pricing U.S. debt next to Greece and Italy at triple B. The gold price may indeed be the canary in the coal mine in regard to U.S. debt and fiscal position.

Chart data as of May 27, 2025. Sources: S&P Capital IQ, Bloomberg, Apollo Chief Economist

Gold Price Theme

- Trump policies drive the growing trend toward nationalism – Foreigners repatriating capital back to home countries – selling both U.S equities and U.S. Treasuries.

- Reality of limited options outside of monetary debasement for dealing with growth of U.S. debt. Trump’s ‘Big Beautiful Bill’ adds to growth of debt and concerns about U.S. fiscal solvency.

- Central Bank bid underpinning gold price as central banks continue accumulation of gold as a neutral asset to counter Western sanctions. Central banks also losing confidence in U.S. Treasuries as a store of value.

- Gold market pricing increasingly shifting to China as Asian market demand overwhelms traditional Western bullion banks’ ability to control price.

- Institutional credibility of Federal Reserve on the line as it deals with public pressure from Trump administration and how it deals with waning interest in U.S. treasury debt, especially on the long end.

Gold Mining Equities Theme

- Gold producers experiencing significant cash flow margins at $3,000 plus gold prices.

- Capital allocation to shareholder returns in the form of buybacks and cash dividends top of mind for investors.

- M&A activity in the precious metals sector remains subdued as managements look to maintain capital discipline despite needing to replenish production pipelines.

- Geopolitical risk, especially West Africa, continues to be discounted.

- Overall investment community yet to appreciate gold miners operating margin expansion and remains significantly underweight in what is already a small sector in grand scheme of market.

e.g., top 15 of the biggest precious metal equities are worth roughly 2% of the Mag-7, in terms of market cap.

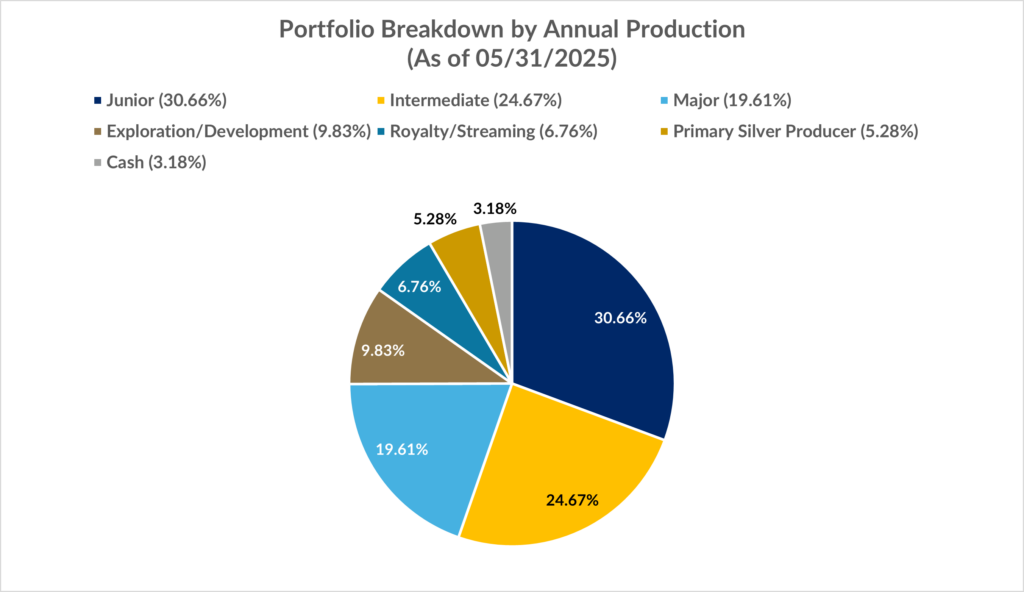

OCM Gold Fund Investment Strategy

The LSEG award-winning* investment strategy OCM has employed is a tiered approach to capture performance as investment flows into the sector move amongst the various subsets of the sector. Typically, capital moves from the senior producers downstream as a bull market in gold matures. Ironically, the major producers, such as Newmont Mining and Barrick Mining, are lagging the gold price move. We expect some catch up by the senior producers as the year goes on and before the next leg higher in the entire sector. See above for our allocation by production profile as of May 31st.

Important Disclosures

Investors should carefully consider the investment objectives, risks, charges, and expenses of the OCM Gold Fund. This and other important information about a Fund are contained in a Fund’s Prospectus, which can be obtained by calling 1-800-779-4681. The Prospectus should be read carefully before investing.

The Fund invests in gold and other precious metals, which involves additional risks, such as the possibility for substantial price fluctuations over a short period of time and may be affected by unpredictable international monetary and political developments such as currency devaluations or revaluations, economic and social conditions within a country, trade imbalances, or trade or currency restrictions between countries. The prices of gold and other precious metals may decline versus the dollar, which would adversely affect the market prices of the securities of gold and precious metals producers. The Fund may also invest in foreign securities which involve greater volatility and political, economic, and currency risks and differences in accounting methods. The Fund is non-diversified, meaning it may concentrate its assets in fewer individual holdings than a diversified fund. Therefore, the Fund is more exposed to individual stock volatility than a diversified fund. Prospective investors who are uncomfortable with an investment that will fluctuate in value should not invest in the Fund.

OCM Gold Fund: Advisors Class Best Fund out of 17 eligible investment companies for the three and five-year periods and 15 eligible investment companies for the ten-year periods ending 11/31/2024 based on consistent annualized total returns.

*The LSEG Lipper Fund Awards, granted annually, highlight funds and fund companies that have excelled in delivering consistently strong risk-adjusted performance relative to their peers. The LSEG Lipper Fund Awards are based on the Lipper Leader for Consistent Return rating, which is a risk adjusted performance measure calculated over 36,60 and 120 months. The fund with the highest Lipper Leader for Consistent Return (Effective Return) value in each eligible classification wins the LSEG Lipper Fund Award. For more information see lipperfundawards.com Although LSEG Lipper makes reasonable efforts to ensure the accuracy and reliability of the data contained herein, the accuracy is not guaranteed by LSEG Lipper

Past performance is no guarantee of future results

There is no guarantee that the Fund will achieve its objective. Diversification does not ensure a profit or guarantee against loss. The prices of securities of gold and precious metals producers have been subject to substantial price fluctuations over short periods of time and may be affected by unpredictable international monetary and political developments, such as currency devaluations or revaluations, economic and social conditions within a country, trade imbalances, or trade or currency restrictions between countries. The prices of gold and other precious metals may decline versus the dollar, which would adversely affect the market prices of the securities of gold and precious metals producers. Because the Fund concentrates its investments in the gold mining industry, a development adversely affecting that industry (for example, changes in the mining laws which increase production costs) would have a greater adverse effect on the Fund than it would if the Fund invested in a number of different industries.

Funds are distributed by Northern Lights, LLC, FINRA/SIPC. Orrell Capital Management, Inc. and Northern Lights Distributors, LLC are not affiliated.