Our 2026 Gold Outlook

It was a historic year for gold and gold assets. Physical gold rose by 64% in 2025, a percentage increase we have not seen in over 40 years. The Philadelphia Gold and Silver Index (XAU), which is an index of precious metal mining companies, rose by over 150% over the same time frame (January 1 – December 31, 2025).

Below are our thoughts for gold’s 2026 potential tailwinds and precious metal equities along with an interview with Schwab Network.

The Big Whales Are Buying (and They Aren’t Selling)

One of the most notable changes in the current market over the last few years is the behavior of global central banks. We are seeing support for the gold price unlike anything witnessed in recent history, as central banks increasingly lose confidence in the U.S. fiscal and monetary policy to support the U.S. dollar as a store of value and, hence, feel underweight in gold holdings.

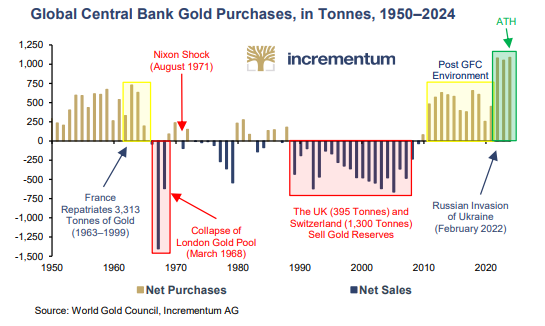

During the gold bull market of the 2000s, Western central banks were predominantly sellers of physical gold, offloading reserves into the market. This selling pressure naturally absorbed some of the global demand. However, the current cycle is marked by a reversal of this trend, as central banks have ceased selling and are accumulating bullion while Western players are relatively uninvolved in the sector.

Adding to this demand is the emergence of non-traditional financial players. We highlight that Tether has been purchasing gold at a rate of roughly two tonnes per week for their new gold backed token named XAUt. When combined with central bank activity, this consistent buying pressure creates a more bullish supply-demand dynamic than investors have seen in previous decades.

(While this Incrementum AG chart is from 2024, it exemplifies that during the 2000s precious metal bull run, global central banks were net sellers of gold)

The Dollar and The Fed: A Question of Independence

Beyond physical demand, our outlook for gold is heavily influenced by the trajectory of the U.S. dollar and monetary policy. We raise questions regarding the Federal Reserve, specifically focusing on what a new chair might mean for the institution’s independence. The core concern is whether monetary policy will increasingly be managed by the federal regime rather than an independent body. If this shift occurs, the implications for the U.S. dollar’s future value are significant, in our opinion. We suggest that if the dollar further depreciates in an attempt to outgrow inflation, there is a good chance gold will continue to rise. Historically, gold has risen with high correlation with U.S. Total Federal Debt Outstanding and its hard for us to believe that number would go down with an even less independent Federal Reserve.

Geopolitical Uncertainty

Geopolitical instability continues to be a primary driver for safe-haven assets. Short-term geopolitical events, in our opinion, do not have a meaningful impact on gold prices. Long-term tensions that impact the value of currencies are our main focus:

• Russia-Ukraine: The unfreezing of Russian assets by the EU and the potential sale of those assets to fund the war effort in Ukraine. Doing so would continue the “weaponization” of the U.S. Dollar.

• US-China Relations: The economic “war” between the U.S. and China is ongoing, as we point specifically to the rare earth sector and the lack of deals thereof—as evidence of this deepening economic divide. To further said divide, China has recently announced they will restrict silver exports for 2026.

• South America: While the U.S. was successful in their quick operation to remove a dictator from power, uncertainty on future U.S. participation in the country looms large with potential for inflationary action.

Precious Metal Miners: Currently Cash Machines

While the macro environment supports the metal, our outlook for mining companies (gold equities) is driven by strong financial performance and the value of ounces in the ground. There are two main value drivers for precious metal mining companies. 1) cash flow generation from existing operations leveraged to higher gold prices and 2) an increase in the value of gold ounces (reserves and resources) in the ground. Both levers are delivering in the current environment.

Major Management

The sector is seeing a refresh in leadership, with new CEOs taking the helm at two of the world’s biggest gold miners, Newmont and Barrick. This has reignited discussions regarding consolidation. Will an acquisition involving Newmont and Barrick finally come to fruition due to the new management’s philosophy or will Barrick break its operation into two or three separate companies going forward?

If a Newmont/Barrick deal were to occur, it would create the largest gold mining company in history. However, the impact would extend beyond just the majors. Lately, the large mergers result have resulted in the divestment of non-core assets. Juniors and intermediate producers that have historically purchased these divested assets have often seen great increases in their share price due to the perception they will put more focus on the asset and how much more impactful these assets are to juniors, on a per-ounce basis.

Show Me The Money

Crowe, C. (Director). (1996). Jerry Maguire [Film still]. TriStar Pictures. [Source: Alamy].Financially, producers are currently generating historic levels of cash flow thanks to their margin expansion. It’s obvious the rising gold price helps but a few inputs are simultaneously going down as well:

• Revenue: The average gold price for the fourth quarter of 2025 was $4,135.20 compared to the $3,464 average price in Q3 2025.

• Costs: While gold prices have risen each quarter this year, major cost inputs like oil and diesel have traded sideways or down during the same period.

Because most producers remain unhedged, they can take full advantage of the current margin expansion. Margin expansion provides optionality that most companies and shareholders alike haven’t enjoyed for years.

M&A Thoughts

Despite robust cash flows, the industry has maintained a relatively conservative approach to growth and M&A. Majors have been conservative, showing a willingness to wait and pay a premium for projects that have been further de-risked rather than aggressively buying early-stage assets. It is our belief that management teams are appropriately hesitant to make the same mistakes made in the 2000s, chasing growth for the sake of growth and ignoring per-share metrics. We view this as bullish for the sector.

The producers are committed to returning capital to shareholders through disciplined buyback programs and dividends. Meanwhile, the exploration sector is seeing a resurgence over the last half of 2025. After funding remained relatively dry for the previous five years, exploration companies are now able to fundraise and progress projects at a quicker rate than in the recent past. Now that projects are being progressed down the development pipeline, it’s possible we will see M&A pick up more quickly than in the past year due to the relatively conservative nature of the larger producers.

Let History be Your Guide: Don’t Fear New Highs

A common concern among investors is that a strong year for an asset class signals an impending correction. However, simply because gold has had a great year, it does not mean it is poised to fall.

For example, look at the multi-year returns of gold seen during the early 1970s. If one had sold their sold at the end of 1972’s great year, one would have missed out on massive gains over the next few years:

1971: 16.37%

1972: 48.74%

1973: 73.49%

1974: 64.04%

(Source: macrotrends.com)

Summary

The convergence of central bank buying, potential changes in U.S. monetary policy, and geopolitical friction provides a strong macro backdrop for gold and gold equities. Simultaneously, the mining sector appears to be in a position of financial strength, characterized by historic cash flows, disciplined capital allocation, and expanding margins. We of course can’t predict what exactly gold or the markets will for the coming year but based on the current information at hand, we are looking forward to 2026.

Schwab Network Interview

Click here or image above to watch.

From Schwab Network: “Greg Orrell notes stablecoins are a new, significant source of demand for gold as the precious metal keeps climbing. “What will be the next demand side to the gold market?” he asks, arguing that he doesn’t see selling catalysts. He explains why investors should consider gold a hedge against “poor policy.” Greg also looks at the health of gold mining companies and how they may try to prolong the life of their mines.”

20260105-5096798

Important Disclosures

Investors should carefully consider the investment objectives, risks, charges, and expenses of the OCM Gold Fund. This and other important information about a Fund are contained in a Fund’s Prospectus, which can be obtained by calling 1-800-779-4681. The Prospectus should be read carefully before investing.The Fund invests in gold and other precious metals, which involves additional risks, such as the possibility for substantial price fluctuations over a short period of time and may be affected by unpredictable international monetary and political developments such as currency devaluations or revaluations, economic and social conditions within a country, trade imbalances, or trade or currency restrictions between countries. The prices of gold and other precious metals may decline versus the dollar, which would adversely affect the market prices of the securities of gold and precious metals producers. The Fund may also invest in foreign securities which involve greater volatility and political, economic, and currency risks and differences in accounting methods. The Fund is non-diversified, meaning it may concentrate its assets in fewer individual holdings than a diversified fund. Therefore, the Fund is more exposed to individual stock volatility than a diversified fund. Prospective investors who are uncomfortable with an investment that will fluctuate in value should not invest in the Fund.

OCM Gold Fund: Advisors Class Best Fund out of 17 eligible investment companies for the three and five-year periods and 15 eligible investment companies for the ten-year periods ending 11/30/2024 based on consistent annualized total returns.

*The LSEG Lipper Fund Awards, granted annually, highlight funds and fund companies that have excelled in delivering consistently strong risk-adjusted performance relative to their peers. The LSEG Lipper Fund Awards are based on the Lipper Leader for Consistent Return rating, which is a risk adjusted performance measure calculated over 36,60 and 120 months. The fund with the highest Lipper Leader for Consistent Return (Effective Return) value in each eligible classification wins the LSEG Lipper Fund Award. For more information see lipperfundawards.com Although LSEG Lipper makes reasonable efforts to ensure the accuracy and reliability of the data contained herein, the accuracy is not guaranteed by LSEG Lipper

Past performance is no guarantee of future results

There is no guarantee that the Fund will achieve its objective. Diversification does not ensure a profit or guarantee against loss. The prices of securities of gold and precious metals producers have been subject to substantial price fluctuations over short periods of time and may be affected by unpredictable international monetary and political developments, such as currency devaluations or revaluations, economic and social conditions within a country, trade imbalances, or trade or currency restrictions between countries. The prices of gold and other precious metals may decline versus the dollar, which would adversely affect the market prices of the securities of gold and precious metals producers. Because the Fund concentrates its investments in the gold mining industry, a development adversely affecting that industry (for example, changes in the mining laws which increase production costs) would have a greater adverse effect on the Fund than it would if the Fund invested in a number of different industries.

Funds are distributed by Northern Lights, LLC, FINRA/SIPC. Orrell Capital Management, Inc. and Northern Lights Distributors, LLC are not affiliated.