OCM Market Perspective

Fed “Independence”

This past week, the Department of Justice issued a subpoena for The Federal Reserve’s (The Fed) chairman, Jerome Powell. The subpoena is for the cost overruns on the Fed’s renovations of their headquarters in Washington D.C.

It is of our opinion, that the subpoena is another tactic by the Trump administration to influence The Fed’s interest rate policy and intimidate Powell. The object of intimidation would be to lower the Fed Funds rate and have Powell step down from the Fed Board of Governors after his chairmanship is up this May (Powell will have two years remaining on his governor position after May 2026).

The implications of continued White House pressure on the monetary policy decision makers are massive. While we have not always believed that the Fed has been truly independent in their decision making, there has been a trust with the bond and equity market that The Fed did not adhere to the will of whoever is in the White House.

Since discontinuing the short lived DODGE project in early 2025, President Trump has been vocal that growth is his chosen path forward to attempt to erase the massive federal debt outstanding. Should Trump have his nomination for chair confirmed and gain control of the Fed Board, it is our opinion that monetary and fiscal policy will be in lockstep. This unity creates a higher likelihood of inflation rising, federal debt outstanding growing, and the U.S. dollar decreasing it’s value further against physical gold.

As we’ve mentioned previously, gold has a high correlation to federal debt outstanding.

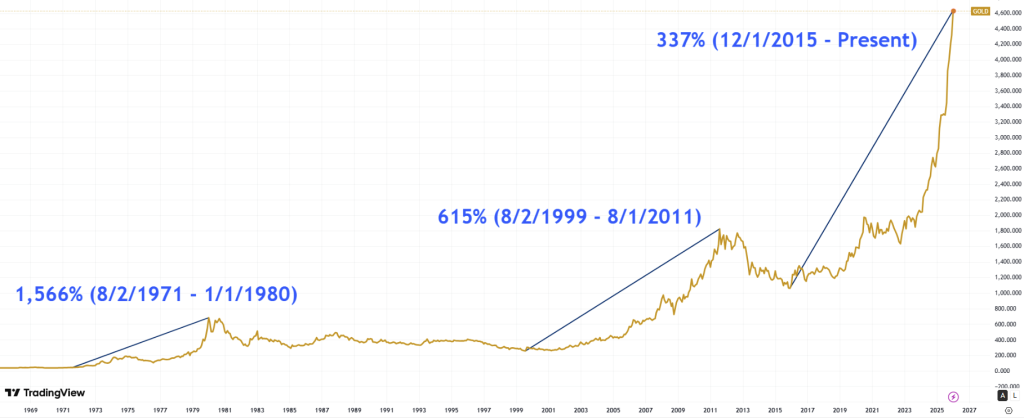

Gold’s Previous Bull Periods

With gold’s positive performance last year, many our questioning what stage we are in with the current precious metal bull cycle.

In our chart above one may observe that the current bull market trails past gold bull runs, on a percentage return basis for one ounce of gold in U.S. dollars.

Where the gold price goes from today over the next 6 months, 1 year, or longer is not for us to proclaim. However, in our opinion, we see much more tailwinds for gold and gold assets over time.

Kitco Mining Interview

Click here or the thumbnail above to watch our interview with Kitco Mining.

Per Kitco Mining:

“Greg Orrell, Portfolio Manager at OCM Gold Fund, joins Kitco Mining’s Paul Harris to break down why the precious metals market enters 2026 in uncharted territory. With gold closing in on $4,500/oz and silver pushing through $80/oz at the time of recording, Orrell highlights how unusual the move has been, noting that “the gold price went up every single month in 2025,” something he says has not happened going back to 1971.

Orrell says the rally reflects a structural shift in demand, led by non-Western buyers and new participants such as Tether, which he says is buying gold on a regular basis. He argues that rising U.S. debt and deficit spending remain the central drivers for gold, while Western investors are still largely on the sidelines. The discussion also explores why silver has entered a new phase, what record margins mean for miners, and why discipline, per-share delivery, and capital returns matter as the cycle evolves.”

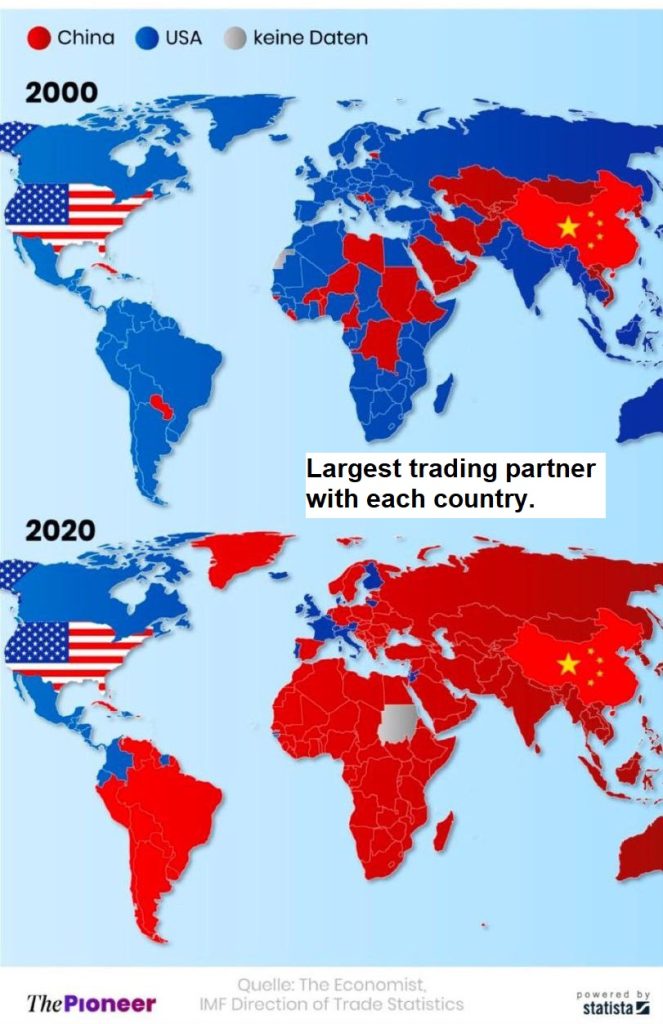

Canada’s Deal with China: Our View

This past week, Canada and China reached a trade deal for electronic vehicles and canola oil, per Reuters. While the deal may not have massive implications on the United States from the onset, it continues a trend represented on the following image.

The map is from 2020 and thus some data may be outdated. However, the overall message is clear that China has gained position as the primary trading partner with many countries across the globe.

Repercussions from less U.S. trade and increased U.S. instability, even on the margins, results in less demand for U.S. dollars and U.S. debt. If the demand for US debt falls, where do the funds flow? It is our opinion, that the rise in the gold price helps answers that question.

For example, Poland announced yesterday that they plan to buy an additional 150 tons, which would increase their reserves to 700 tons. Poland central bank management board member Artur Sobon told Bloomberg News “The price is not a primary consideration for us.”

Important Disclosures

Investors should carefully consider the investment objectives, risks, charges, and expenses of the OCM Gold Fund. This and other important information about a Fund are contained in a Fund’s Prospectus, which can be obtained by calling 1-800-779-4681. The Prospectus should be read carefully before investing.

The Fund invests in gold and other precious metals, which involves additional risks, such as the possibility for substantial price fluctuations over a short period of time and may be affected by unpredictable international monetary and political developments such as currency devaluations or revaluations, economic and social conditions within a country, trade imbalances, or trade or currency restrictions between countries. The prices of gold and other precious metals may decline versus the dollar, which would adversely affect the market prices of the securities of gold and precious metals producers. The Fund may also invest in foreign securities which involve greater volatility and political, economic, and currency risks and differences in accounting methods. The Fund is non-diversified, meaning it may concentrate its assets in fewer individual holdings than a diversified fund. Therefore, the Fund is more exposed to individual stock volatility than a diversified fund. Prospective investors who are uncomfortable with an investment that will fluctuate in value should not invest in the Fund.

Past performance is no guarantee of future results

There is no guarantee that the Fund will achieve its objective. Diversification does not ensure a profit or guarantee against loss. The prices of securities of gold and precious metals producers have been subject to substantial price fluctuations over short periods of time and may be affected by unpredictable international monetary and political developments, such as currency devaluations or revaluations, economic and social conditions within a country, trade imbalances, or trade or currency restrictions between countries. The prices of gold and other precious metals may decline versus the dollar, which would adversely affect the market prices of the securities of gold and precious metals producers. Because the Fund concentrates its investments in the gold mining industry, a development adversely affecting that industry (for example, changes in the mining laws which increase production costs) would have a greater adverse effect on the Fund than it would if the Fund invested in a number of different industries.

Funds are distributed by Northern Lights, LLC, FINRA/SIPC. Orrell Capital Management, Inc. and Northern Lights Distributors, LLC are not affiliated.